Results from ServiceNow (NASDAQ: NOW) bode well for cloud services stocks. The company posted results that sparked a round of surprisingly bullish chatter from analysts that points to continued strength in this and other cloud services names.

Analysts viewed the ServiceNow results as remarkably strong, defying expectations on broad demand, with significant improvement in the outlook all because of AI. AI is expected to and is already proving capable of generating substantial cost savings for businesses; it will only gain momentum and drive business in the cloud. Because many of these stocks are beaten down on depressed expectations, there is a significant opportunity for them to outperform expectations and reinvigorate their stock prices.

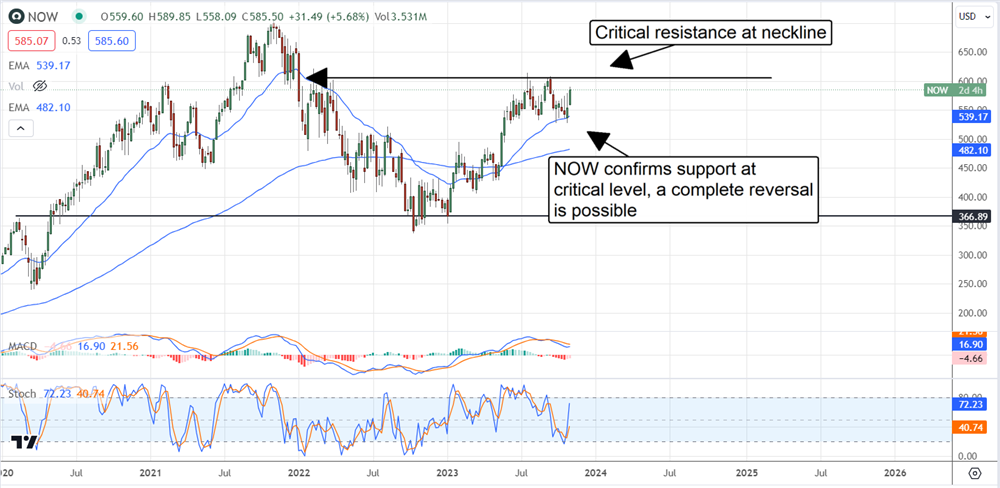

ServiceNow confirms reversal, leads cloud stocks higher

ServiceNow had a strong quarter, with net revenues up 25% compared to last year. The $2.92 billion in revenue beat consensus by about 100 basis points on strength in government spending and AI, with revenue in that segment up 75%. Total subscription revenue is up 27%, outpacing the consensus by several hundred basis points, with the remaining performance obligation up an equal amount.

Guidance is what has ServiceNow stock moving higher. The company raised its guidance for the year, and it may be cautious. A new partnership with Deloitte highlights the growth potential; Deloitte will embed ServiceNow generative AI into its OperateEdge platform, and other large clients are doing likewise. Growth of large clients topped 50% for the quarter, and the penetration is deepening to provide a dual tailwind for growth.

Analysts rate this stock a Moderate Buy and have been raising their price targets all year. The Q3 release sparked another round of revisions, with the consensus target up 3% compared to last quarter and 12% compared to last year but in alignment with recent price action. The takeaway is that recent price targets have the stock trading in the $650 to $700 range, which is 7% to 15% above current action.

Datadog in the doghouse; market ready to rebound

Datadog (NASDAQ: DDOG) shares sank more than 20% following the Q2 release on overreacting to mixed news. The Q2 results were better than expected but came with mixed guidance that included modestly weak top-line expectations but better-than-expected earnings. The takeaway is that revenue weakness will be offset by earnings strength, and both targets may be cautious; Datadog raised guidance significantly in Q1, the Q2 reduction is a minor give-back, and outperformance is typical. Regarding next year, analysts project 25% top-line growth and a wider margin.

The analysts are expecting good things in Q3 2023 despite the guidance cut. They have only raised their revenue and earnings targets since the Q2 release and have consensus pegged near the top of the range. They’ve also been lowering their price targets for the stock, putting it on the Most Downgraded stock list. This activity has the market trading at a critical level and well positioned for a rebound, given a solid report. Despite the downward revisions, analysts see this market advancing more than 20%.

Snowflake: a blizzard of opportunity in AI

Snowflake (NASDAQ: SNOW) is another cloud stock whose share price is struggling to gain traction despite the massive opportunity in AI. The company’s growth slowed in 2023, helping to cap share price gains, but an acceleration of business is expected next year that will bring significant earnings leverage. The growth driver for this company is the need for data and data management, an absolute requirement for creating, training, deploying, and utilizing AI.

The company is embedding AI services across its platform to help businesses manage and gain insight from their data. To that end, Snowflake acquired several AI-oriented businesses to help with searching at scale and applying AI models.

Snowflake earnings are expected to grow by 50% in 2024, and the bar is likely low. Analysts have been lowering their targets despite persistent high-double-digit growth in large clients and a remarkable 142% net retention rate. This company is growing its client base and deepening penetration in what many see as the first innings of the AI revolution, so outperformance is more likely than not. As it is, revenue growth is estimated to slow to 28% from 35% in Q3 2023.