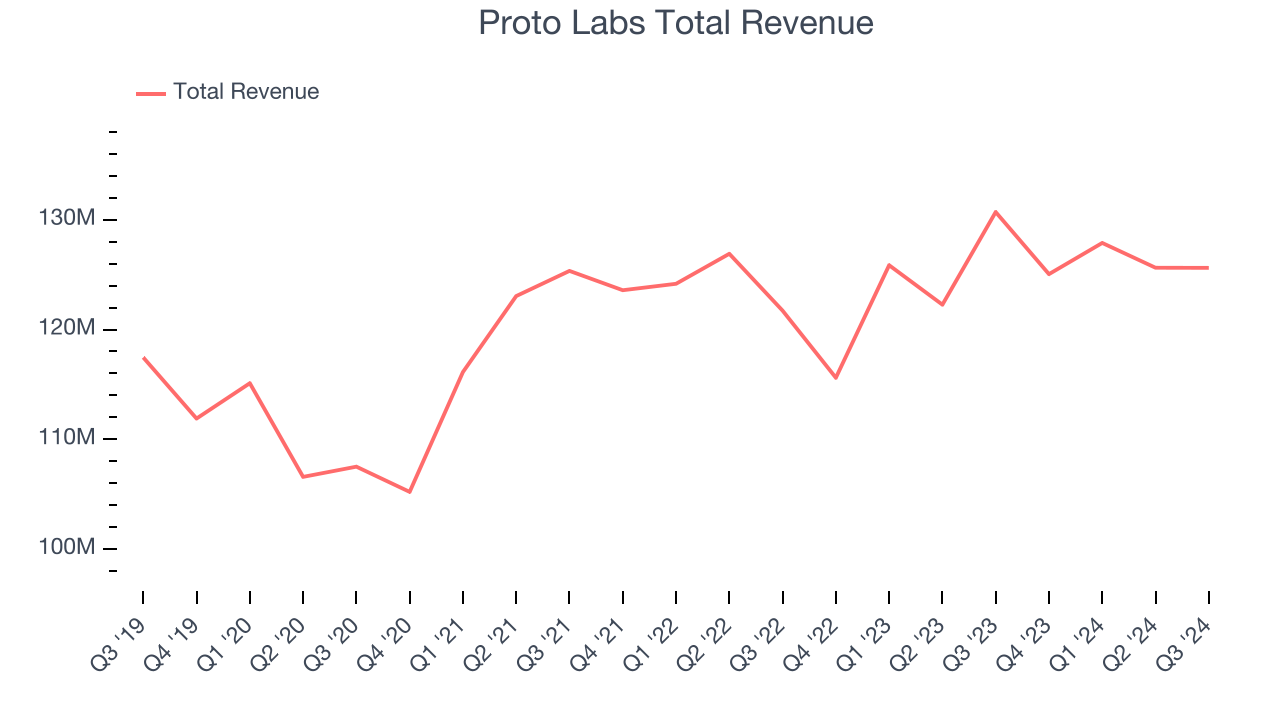

Manufacturing services provider Proto Labs (NYSE:PRLB) reported Q3 CY2024 results topping the market’s revenue expectations, but sales fell 3.9% year on year to $125.6 million. On the other hand, the company expects next quarter’s revenue to be around $119 million, slightly below analysts’ estimates. Its non-GAAP profit of $0.47 per share was also 46% above analysts’ consensus estimates.

Is now the time to buy Proto Labs? Find out by accessing our full research report, it’s free.

Proto Labs (PRLB) Q3 CY2024 Highlights:

- Revenue: $125.6 million vs analyst estimates of $121.4 million (3.5% beat)

- Adjusted EPS: $0.47 vs analyst estimates of $0.32 (46% beat)

- EBITDA: $21.86 million vs analyst estimates of $17.46 million (25.2% beat)

- Revenue Guidance for Q4 CY2024 is $119 million at the midpoint, below analyst estimates of $120 million

- Adjusted EPS guidance for Q4 CY2024 is $0.32 at the midpoint, above analyst estimates of $0.29

- Gross Margin (GAAP): 45.6%, in line with the same quarter last year

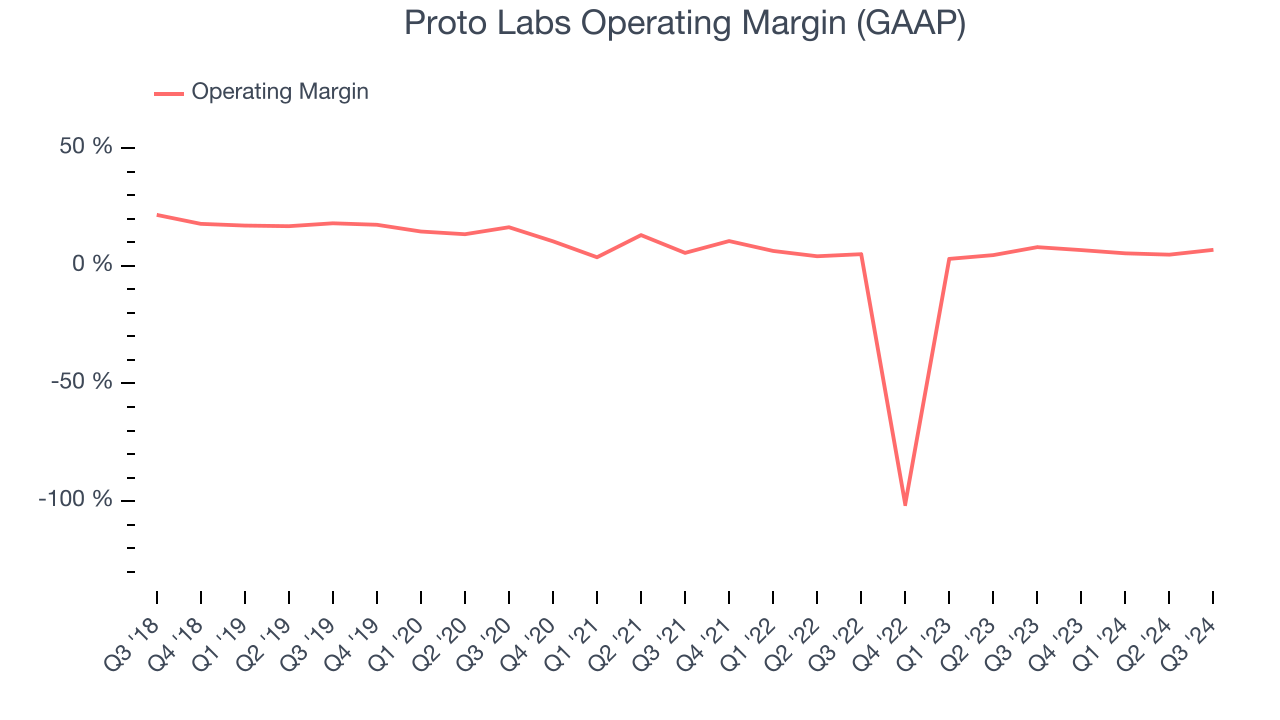

- Operating Margin: 6.8%, down from 8% in the same quarter last year

- EBITDA Margin: 17.4%, in line with the same quarter last year

- Free Cash Flow Margin: 18.5%, up from 16.2% in the same quarter last year

- Market Capitalization: $689 million

"Our disciplined approach and resilient business model drove solid financial results in the third quarter, despite continued dynamic challenges in the manufacturing sector," said Rob Bodor, President and Chief Executive Officer.

Company Overview

Pioneering the concept of online quoting and manufacturing for custom prototypes and low-volume production parts, Proto Labs (NYSE:PRLB) offers injection molding, 3D printing, and sheet metal fabrication for manufacturers in various industries.

Custom Parts Manufacturing

Onshoring and inventory management–themes that grew in focus after COVID wreaked havoc on global supply chains–are tailwinds for companies that combine economies of scale with reliable service. Many in the space have adopted 3D printing to efficiently address the need for bespoke parts and components, but all companies are still at the whim of economic cycles. For example, consumer spending and interest rates can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

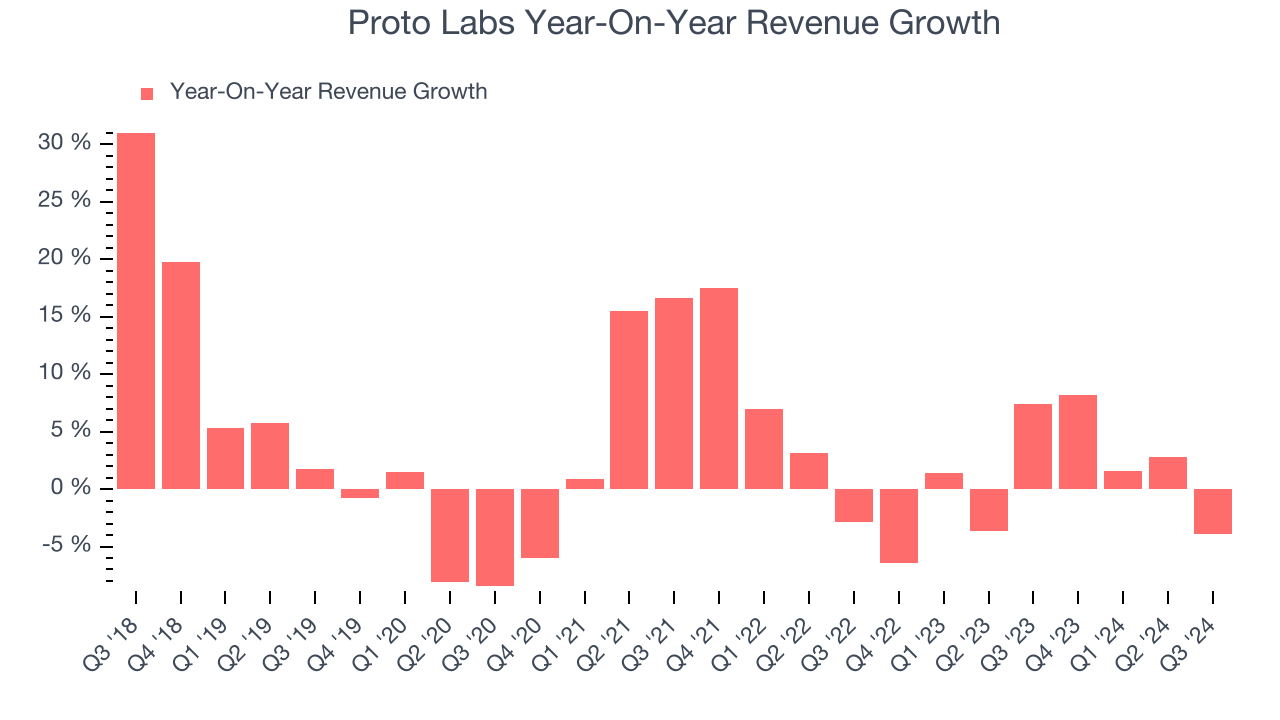

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Proto Labs’s 1.9% annualized revenue growth over the last five years was sluggish. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Proto Labs’s recent history shows its demand slowed as its revenue was flat over the last two years.

We can better understand the company’s revenue dynamics by analyzing its three most important segments: Injection Molding , CNC Machining , and 3D Printing, which are 37.3%, 42.5%, and 17.1% of revenue. Over the last two years, Proto Labs’s Injection Molding revenue (injection molds and parts) averaged 1.9% year-on-year declines, but its CNC Machining (custom CNC-machined parts) and 3D Printing (custom 3D-printed parts) revenues averaged 4.4% and 4.1% growth.

This quarter, Proto Labs’s revenue fell 3.9% year on year to $125.6 million but beat Wall Street’s estimates by 3.5%. Management is currently guiding for a 4.8% year-on-year decline next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and shows the market believes its products and services will face some demand challenges.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Proto Labs was profitable over the last five years but held back by its large cost base. Its average operating margin of 3% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

Looking at the trend in its profitability, Proto Labs’s annual operating margin decreased by 9.6 percentage points over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Proto Labs generated an operating profit margin of 6.8%, down 1.1 percentage points year on year. Since Proto Labs’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

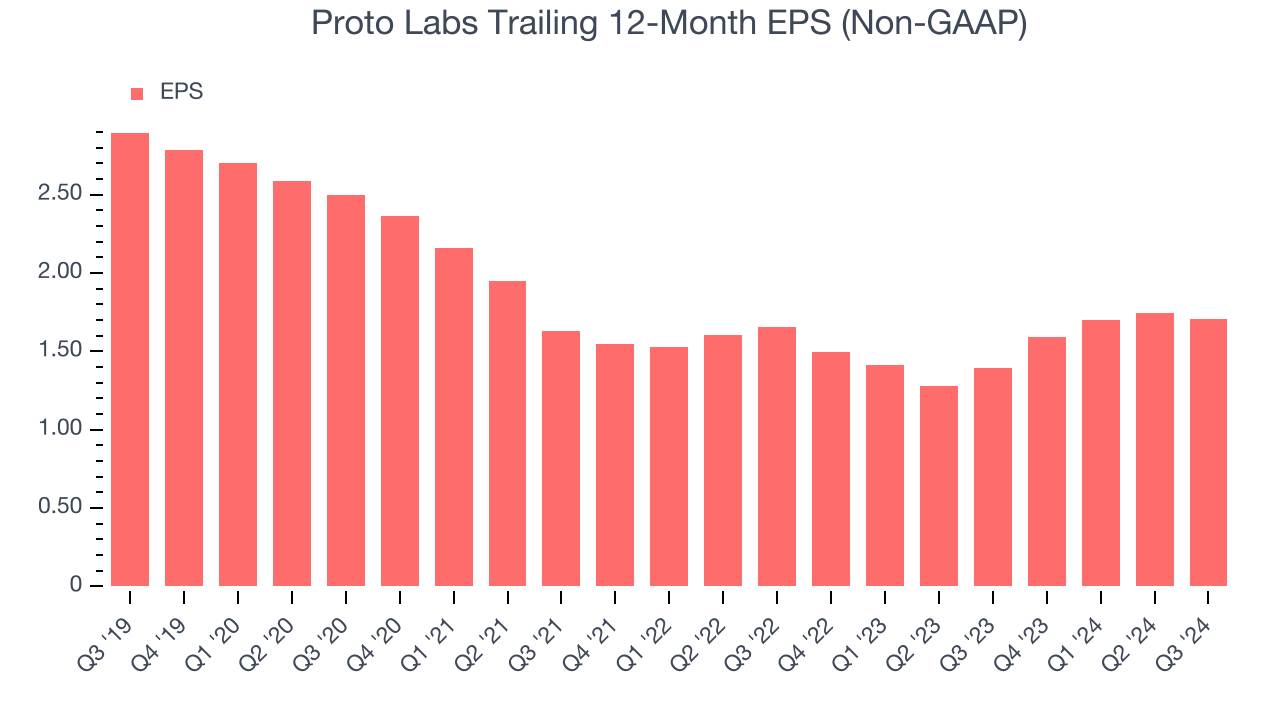

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Sadly for Proto Labs, its EPS declined by 10% annually over the last five years while its revenue grew by 1.9%. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Proto Labs’s earnings to better understand the drivers of its performance. As we mentioned earlier, Proto Labs’s operating margin declined by 9.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

For Proto Labs, its two-year annual EPS growth of 1.6% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.In Q3, Proto Labs reported EPS at $0.47, down from $0.51 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Proto Labs’s full-year EPS of $1.71 to shrink by 20.7%.

Key Takeaways from Proto Labs’s Q3 Results

The company beat across the board this quarter, including revenue, EBITDA, and EPS. EPS guidance for next quarter was also ahead. On the other hand, its revenue guidance for next quarter missed slightly. Zooming out, we think this was still a solid quarter, and the market seems to be forgiving the small guidance shortfall. The stock traded up 17.2% to $32.10 immediately after reporting.

Proto Labs put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.