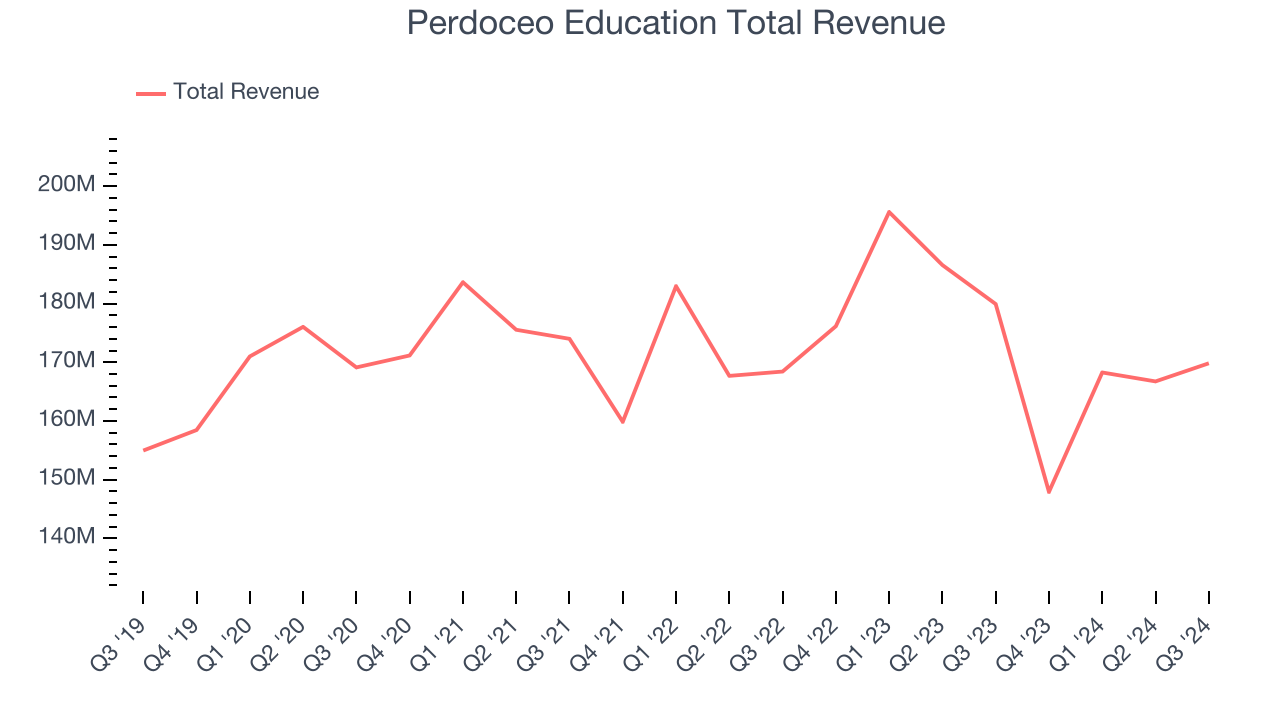

Higher education company Perdoceo Education (NASDAQ:PRDO) beat Wall Street’s revenue expectations in Q3 CY2024, but sales fell 5.6% year on year to $169.8 million. Its non-GAAP profit of $0.59 per share was also 11.3% above analysts’ consensus estimates.

Is now the time to buy Perdoceo Education? Find out by accessing our full research report, it’s free.

Perdoceo Education (PRDO) Q3 CY2024 Highlights:

- Revenue: $169.8 million vs analyst estimates of $164.6 million (3.2% beat)

- Adjusted EPS: $0.59 vs analyst estimates of $0.53 (11.3% beat)

- EBITDA: $47.85 million vs analyst estimates of $48 million (small miss)

- Management raised its full-year Adjusted EPS guidance to $2.26 at the midpoint, a 3.4% increase

- Gross Margin (GAAP): 83.3%, in line with the same quarter last year

- Operating Margin: 26.4%, down from 28% in the same quarter last year

- EBITDA Margin: 28.2%, down from 30.2% in the same quarter last year

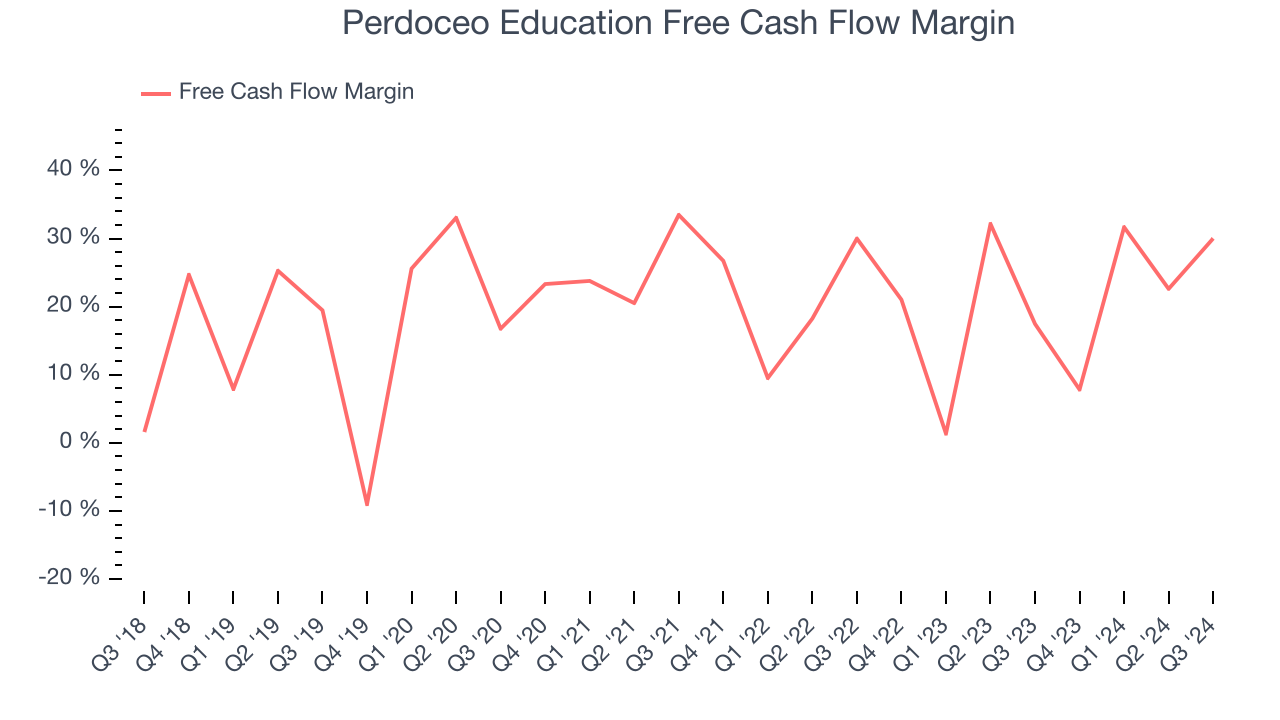

- Free Cash Flow Margin: 30%, up from 17.5% in the same quarter last year

- Market Capitalization: $1.67 billion

"Operating performance for the quarter was ahead of our expectations as both academic institutions continued to experience strong student retention and engagement through the quarter,” said Todd Nelson, President and Chief Executive Officer.

Company Overview

Formerly known as Career Education Corporation, Perdoceo Education (NASDAQ:PRDO) is an educational services company that specializes in postsecondary education.

Education Services

A whole industry has emerged to address the problem of rising education costs, offering consumers alternatives to traditional education paths such as four-year colleges. These alternative paths, which may include online courses or flexible schedules, make education more accessible to those with work or child-rearing obligations. However, some have run into issues around the value of the degrees and certifications they provide and whether customers are getting a good deal. Those who don’t prove their value could struggle to retain students, or even worse, invite the heavy hand of regulation.

Sales Growth

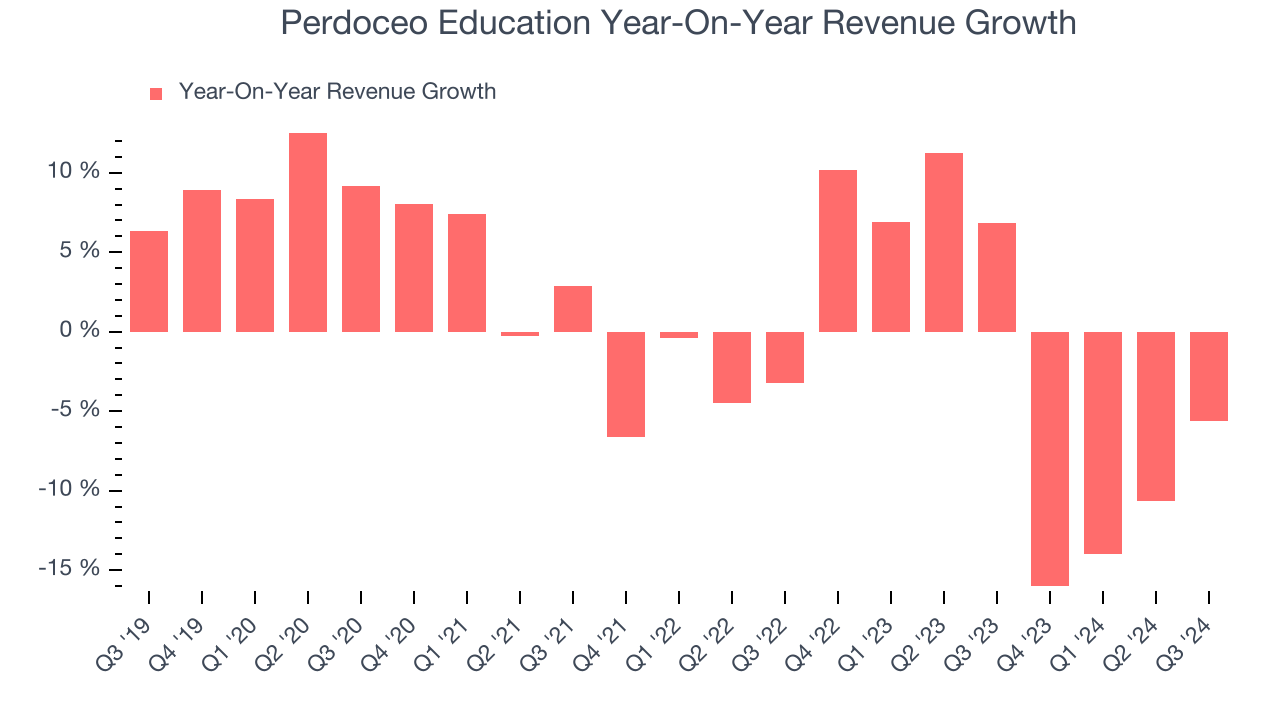

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Unfortunately, Perdoceo Education’s 1.2% annualized revenue growth over the last five years was weak. This fell short of our expectations and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Perdoceo Education’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.9% annually.

This quarter, Perdoceo Education’s revenue fell 5.6% year on year to $169.8 million but beat Wall Street’s estimates by 3.2%.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Perdoceo Education has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 20.5% over the last two years, quite impressive for a consumer discretionary business.

Perdoceo Education’s free cash flow clocked in at $50.98 million in Q3, equivalent to a 30% margin. This result was good as its margin was 12.6 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Key Takeaways from Perdoceo Education’s Q3 Results

It was great to see Perdoceo Education’s strong EPS forecast for next quarter, which exceeded analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 5.8% to $26.30 immediately following the results.

Perdoceo Education put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.