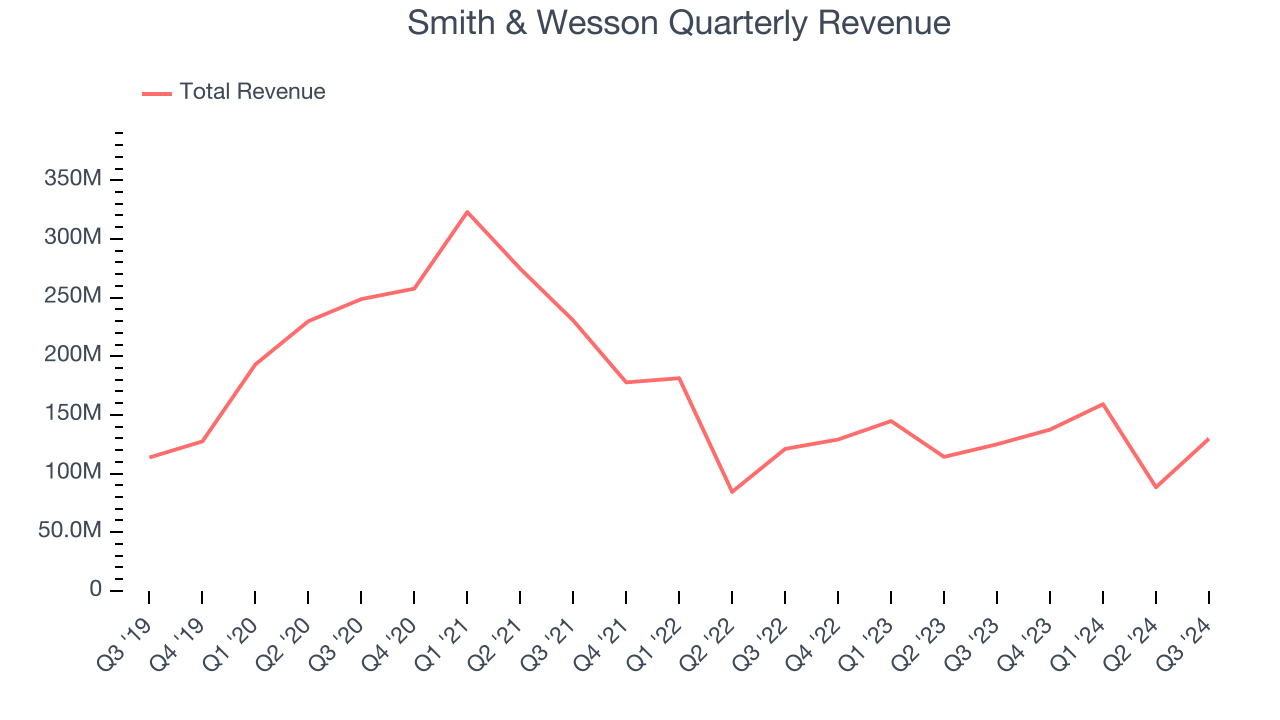

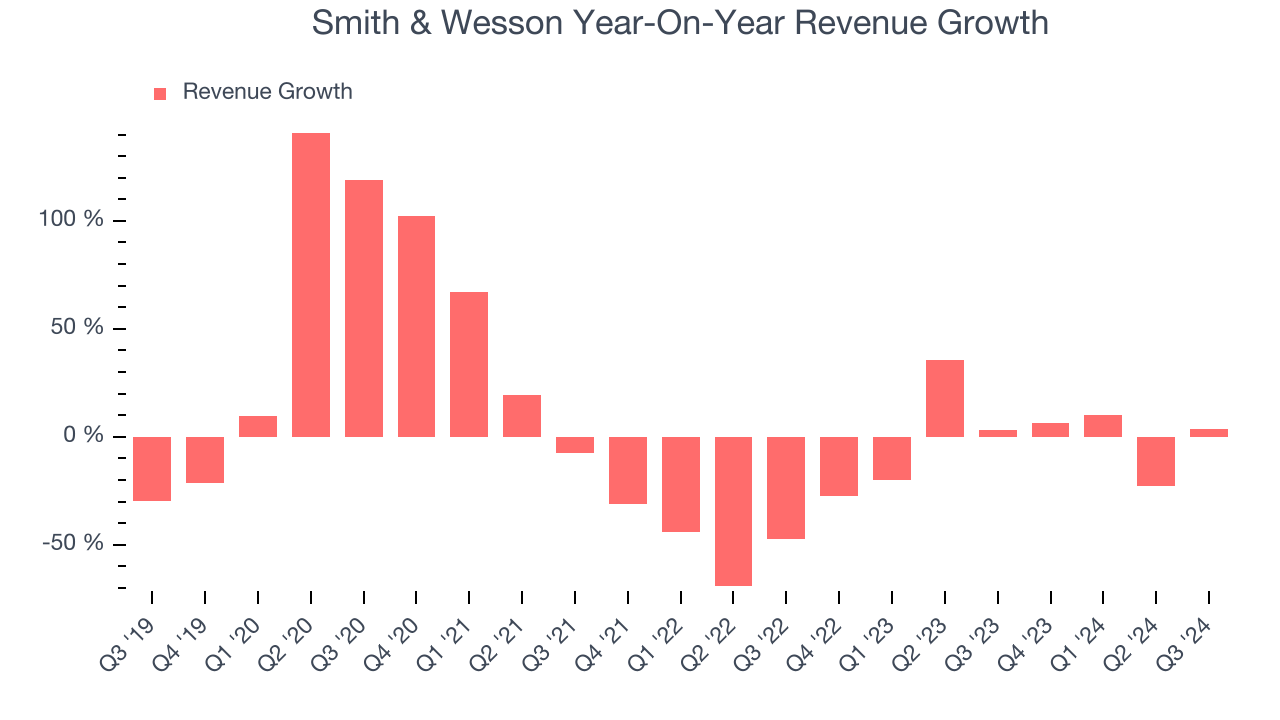

American firearms manufacturer Smith & Wesson (NASDAQ:SWBI) missed Wall Street’s revenue expectations in Q3 CY2024 as sales rose 3.8% year on year to $129.7 million. Its non-GAAP profit of $0.11 per share was 33.3% below analysts’ consensus estimates.

Is now the time to buy Smith & Wesson? Find out by accessing our full research report, it’s free.

Smith & Wesson (SWBI) Q3 CY2024 Highlights:

- Revenue: $129.7 million vs analyst estimates of $133.5 million (3.8% year-on-year growth, 2.9% miss)

- Adjusted EPS: $0.11 vs analyst expectations of $0.17 (33.3% miss)

- Adjusted EBITDA: $18.49 million vs analyst estimates of $20.62 million (14.3% margin, 10.3% miss)

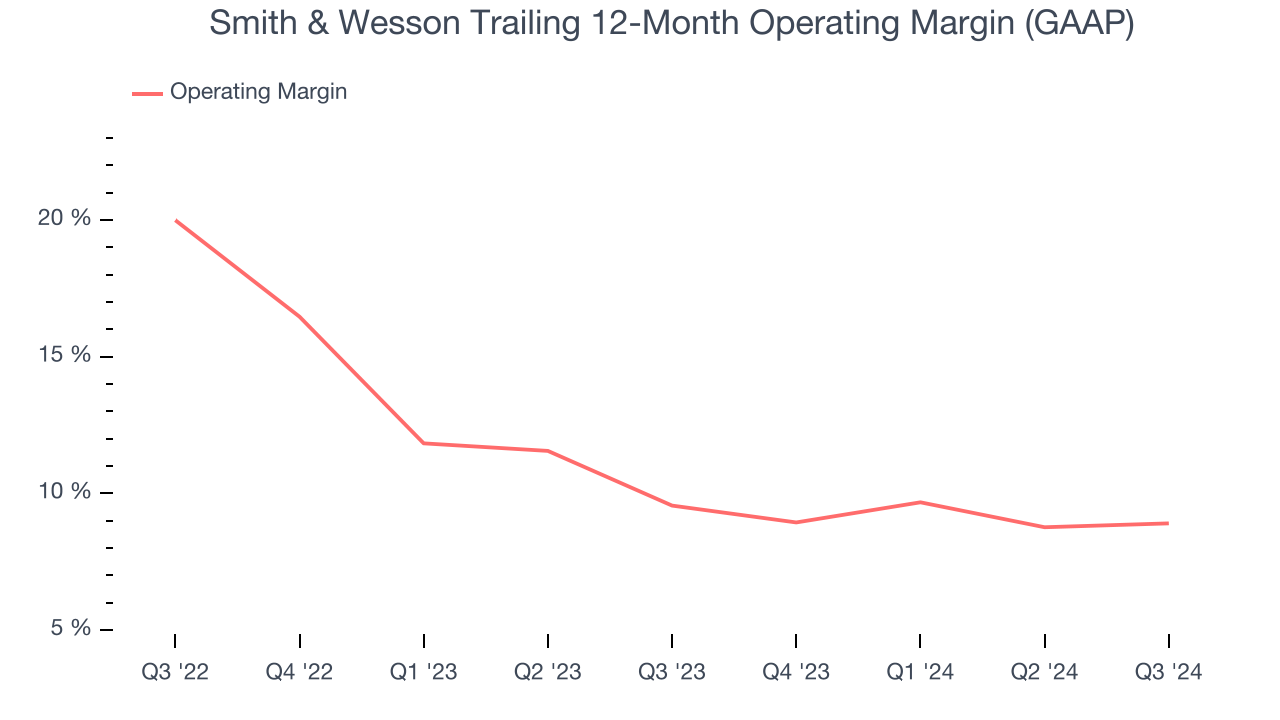

- Operating Margin: 5.4%, in line with the same quarter last year

- Free Cash Flow was -$10.7 million compared to -$37.87 million in the same quarter last year

- Market Capitalization: $632.4 million

Company Overview

With a history dating back to 1852, Smith & Wesson (NASDAQ:SWBI) is a firearms manufacturer known for its handguns and rifles.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Smith & Wesson’s demand was weak and its revenue declined by 1.2% per year. This was below our standards and signals it’s a lower quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Smith & Wesson’s recent history shows its demand has stayed suppressed as its revenue has declined by 4.5% annually over the last two years.

This quarter, Smith & Wesson’s revenue grew by 3.8% year on year to $129.7 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 12.4% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Smith & Wesson’s operating margin might have seen some fluctuations over the last 12 months but has remained more or less the same, averaging 9.2% over the last two years. This profitability was mediocre for a consumer discretionary business and caused by its suboptimal cost structure.

In Q3, Smith & Wesson generated an operating profit margin of 5.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Key Takeaways from Smith & Wesson’s Q3 Results

We struggled to find many resounding positives in these results as its revenue, EPS, and EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 12.8% to $11.90 immediately after reporting.

Smith & Wesson’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.