Three Gold Miners To Buy On Dips

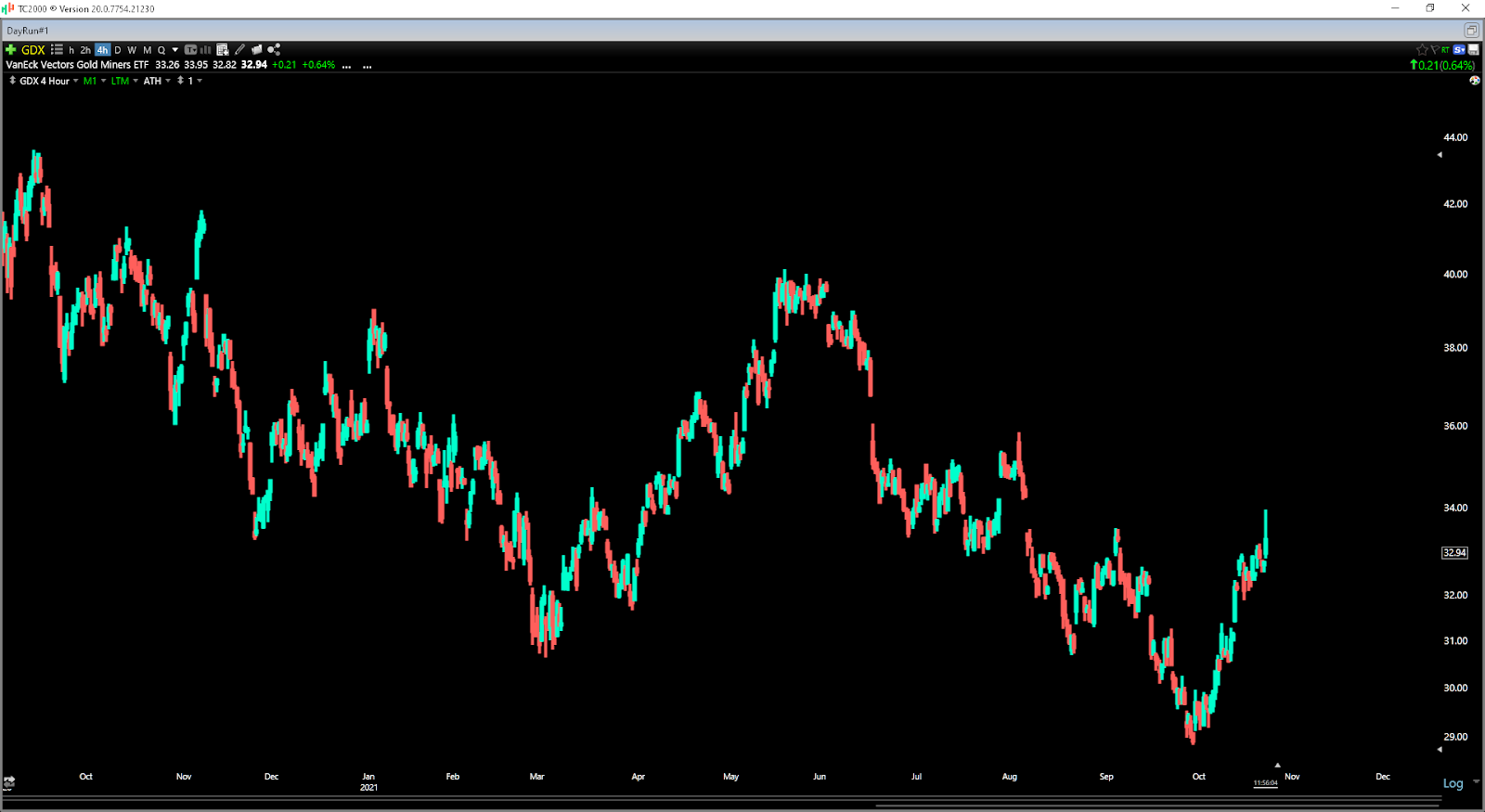

After a brutal year for the precious metals space, we’re finally seeing some signs of life, with the Gold Miners Index (GDX) up over 10% thus far this month. This strong recovery is not surprising given that we saw miners trading at their most attractive valuation levels in years last month, with many producers trading at deep discounts to their net asset value. However, valuations across the space are still very compelling despite the recent rally, suggesting that any sharp pullbacks should present low-risk buying opportunities. In this update, we’ll look at three of the highest-quality names that are worth keeping at the top of one’s shopping list:

(Source: TC2000.com)

One of the favored ways to play the gold price (GLD) is the Gold Miners Index, given that it provides exposure to the index with minimal specific company risk, given that the ETF holds over 50 names, with no weighting above 9%. However, given that the average million-ounce producer pays a dividend yield above 2.8%, I see the individual miners as much more attractive, though one’s stock selection within the sector is paramount. The key to success with this strategy is looking for the best names that have fallen out of favor and are trading at a discount to their net asset value. When it comes to the best mix for upside exposure while controlling volatility, the ideal spread is a combination of producers and developers, with a heavier weighting in the mid-cap names. Among this group, names that meet these criteria that look like solid buy-the-dip candidates are SilverCrest Metals (SILV), Pretium Resources (PVG), and Yamana Gold (AUY).

Beginning with SilverCrest Metals, the company is a silver developer currently busy constructing its silver-gold mine in Mexico. Once construction is complete next year, SilverCrest expects to produce more than 10 million silver-equivalent ounces [SEOs] per year at industry-leading all-in sustaining costs [AISC] of ~$7.00/oz. This will make the company one of the highest-margin producers sector-wide beginning in 2023, with margins projected to come in at 70% margins at a silver price of $25.50/oz. This allows SILV to generate significant free cash flow in periods of metals price strength and provides defense against weakness in metals price. In fact, even with silver prices below $21.00/oz, SILV can still churn out more than $100 million in free cash flow per annum.

(Source: Company Presentation)

At a current enterprise value of ~$1.0 billion, SilverCrest is quite reasonably valued, especially after suffering a more than 25% correction. The high-grade silver developer currently has a resource base of approximately 140 million SEOs, with 95 million SEOs in its current mine plan. Based on these figures, SILV trades at an enterprise value per silver-equivalent ounce of ~$7.15. Ultimately believe that SILV’s resources can grow to more than 185 million SEOs by 2024, given that it has a regional property that it is currently drilling, and it has uncovered its 140 million SEO resource base among just 15 veins of the 45 identified on its property. Based on a resource base of 185 million SEOs, SILV’s enterprise value per ounce drops to a mere $5.40/oz, which is a very reasonable figure for a company capable of processing each SEO for a cost of less than $7.50, leaving more than $16.00/oz in profit.

(Source: SilverCrest Metals Presentation)

From a financial standpoint, the valuation is even more compelling, with SILV trading at an estimated 11% free cash flow yield in FY2023, despite having some of the highest margins sector-wide. At a current share price of $8.00, I am not in a rush to start a position in the stock, given that it has rallied sharply over the past two weeks. However, if we were to see a pullback below $7.10, where SILV’s FY2023 free cash flow yield would increase to closer to 13%, I would view this as a low-risk buying opportunity.

Moving to the first producer on the list, Pretium, the stock actually bottomed out well ahead of its peer group in early August, while the GDX made its low in late September. The company has had a solid year thus far, both operationally and financially, with outstanding near-mine drill results and continued cost control at its Brucejack Mine in Canada. During the most recent quarter, Pretium produced ~83,100 ounces of gold despite COVID-19 related headwinds and is well on track to meet its annual guidance.

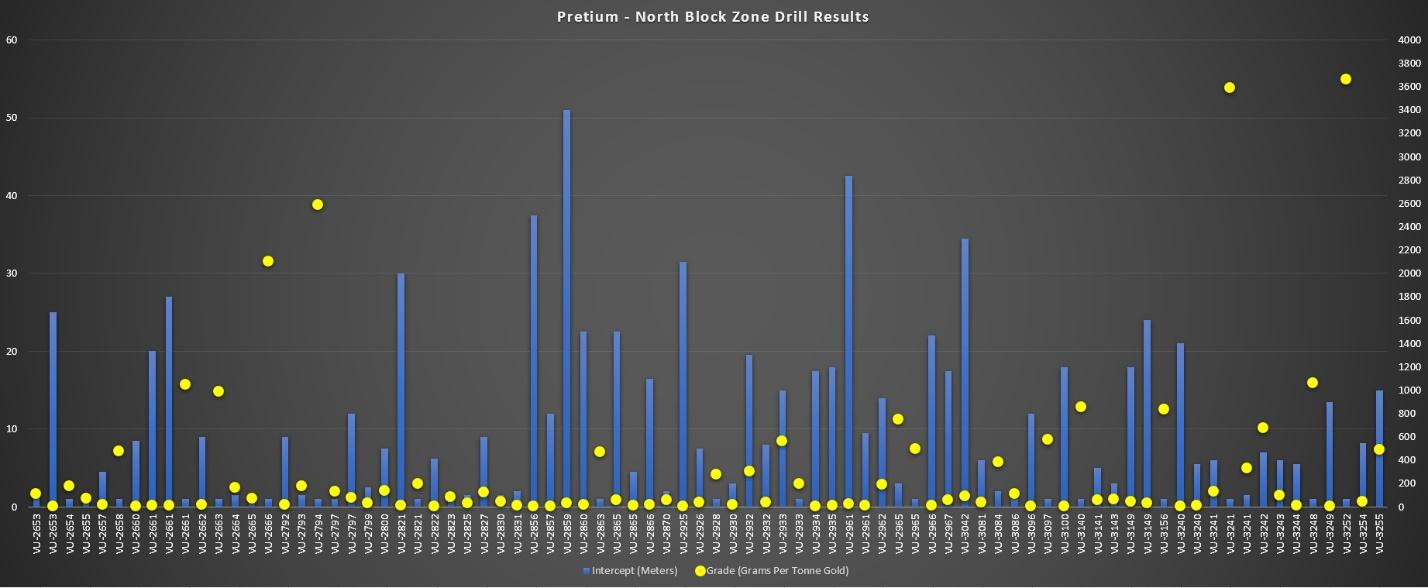

(Source: Company Filings, Author’s Chart)

From an exploration standpoint, Pretium looks set up to deliver meaningful growth in its resources, with highlight intercepts that include 15 meters of 493 grams per tonne gold, 7 meters of 676 grams per tonne gold, and 34 meters of 93.4 grams per tonne gold. These are some of the best intercepts released sector-wide over the past few years and are well above Pretium’s average reserve grade of 8.7 grams per tonne gold. Assuming exploration success continues, PVG looks like it should be able to extend its mine life at Brucejack, both with higher grades near-mine and bulk tonnage mineralization at its Hanging Glacier Target, which sits less than 10 kilometers from its processing plant.

While annual earnings per share expected to decline year-over-year for PVG, which is not ideal, this is mostly due to being up against tough comps in the year-ago period. The good news is that PVG is on track to increase annual EPS by more than 30% next year to $0.88 per share, which leaves the stock trading at a very reasonable valuation of less than 13x earnings at a share price of $11.30. Similar to SILV, I am not in a rush to add to my position in PVG here, given that the stock is up over 20% in the past three weeks. However, if PVG were to pull back below the $10.30 level, I would view this as a low-risk buying opportunity.

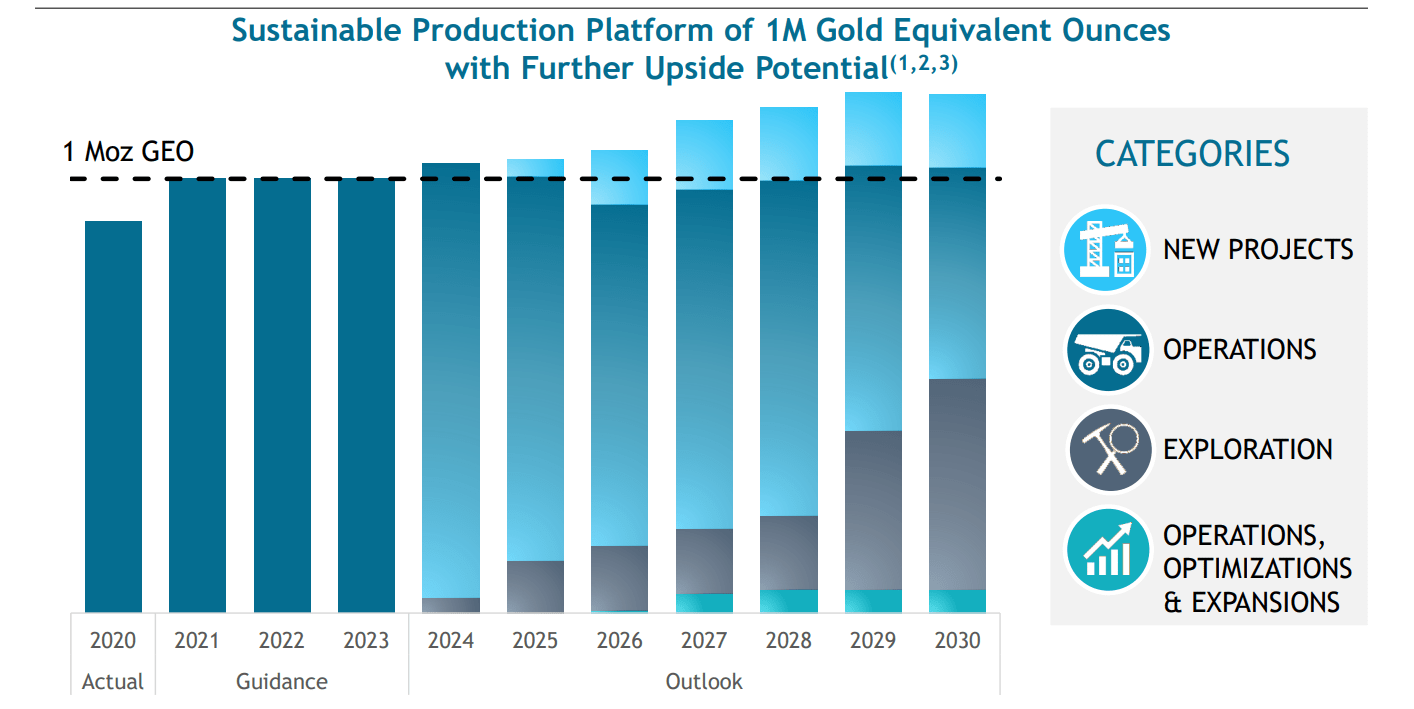

Finally, the last name on the list is Yamana Gold, a million-ounce producer with a strong track record of dividend growth, with its dividend being raised by another 12% just recently. This marked the company’s sixth dividend increase in the past two years, with the dividend now sitting at $0.12 per share and now up 500% on a two-year basis. Since Yamana sold its Chapada Mine in 2018, the company has continued to turn its business around and has made growth a priority while also looking to shed its heavy debt load. These efforts are paying off, with AUY having an attractive organic growth project in Wasamac, the ability to increase production meaningfully at its Jacobina Mine. At the same time, the company is waiting for potential production from its massive MARA Project, where it has a partnership.

(Source: Yamana Gold Company Presentation)

Assuming the first two mines come online by FY2025, AUY could increase its production profile from 1 million gold-equivalent ounces per annum to 1.2 million gold-equivalent ounces. If we look out further, production could increase further to 1.35 million gold-equivalent ounces by 2027, with these ounces expected to come at much lower costs. One, it will provide a significant boost to AUY’s annual revenue and free cash flow due to increased sales at higher margins. Two, it will bolster the company’s balance sheet, allowing AUY to continue to invest aggressively in exploration and smaller acquisitions to continue to grow its production profile. Based on estimated FY2023 annual earnings per share of $0.35, AUY trades at a dirt-cheap valuation of just 12x earnings while paying an attractive 2.80% yield. So, I see the stock as a buy on any weakness for investors looking for a mix of growth and value.

The GDX is the most hated it’s been in years, but we are finally seeing signs of a potential turnaround, and the valuations are rarely this attractive. This is providing investors with a low-risk opportunity to diversify their exposure from more expensive sectors while also picking up a solid yield in the process, with names like AUY. In summary, while I am not currently adding new exposure, I plan to continue adding exposure to miners if we see some weakness over the coming weeks. As noted above, SILV looks like a low-risk buy below $7.10, while PVG looks like a low-risk buy at $10.30 or lower. For Yamana Gold, I see the stock as a core holding and find it attractive below $4.30 per share.

Disclosure: I am long GLD, AUY, PVG

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

GDX shares were trading at $33.07 per share on Friday afternoon, up $0.34 (+1.04%). Year-to-date, GDX has declined -8.19%, versus a 22.30% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Gold Miners to Consider Buying on the Dip appeared first on StockNews.com