It's been an incredible year thus far for the Nasdaq Composite (COMPQ), with the index up more than 16% year-to-date and many tech stocks up as much as 50%. This relentless rally has made it difficult to find growth at a reasonable price and also challenging to find names that aren't extended from recent breakouts. However, while most names are un-investable at current levels, this is an opportune time to begin building shopping lists. This is because it's quite possible we could see a correction before year-end to wring out some of the excess bullish sentiment, and it's always better to be prepared ahead of time. In this update, we'll look at two attractive tech names with industry-leading growth rates and ideal buy points if we do get a sharp correction:

(Source: TC2000.com)

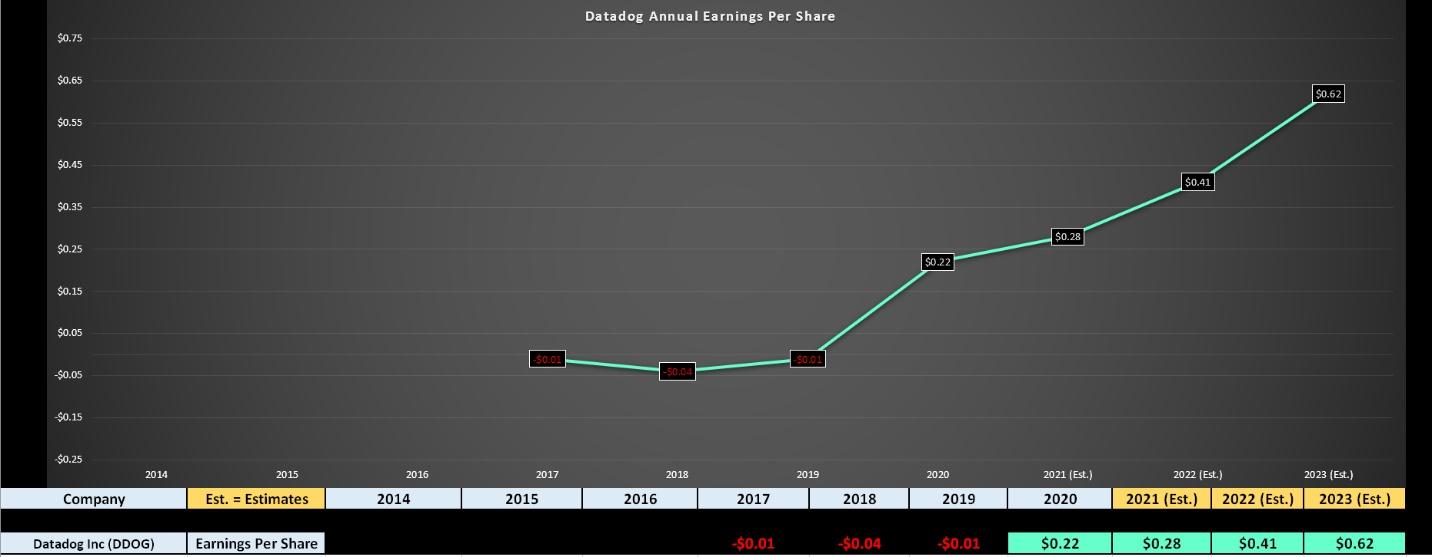

Unity Software (U) and Datadog (DDOG) are both in the Software industry group, and both have posted strong quarter-to-date performance, easily outperforming their tech peers. While Datadog is a data observability service for cloud-scale applications, Unity is a video-game software development company founded in Denmark. With revenue growth rates of 67% year-over-year and 48% year-over-year, respectively, both companies are seeing exceptional growth and are in the sweet spot from an institutional investment standpoint. This is because Datadog just turned profitable last year with positive annual earnings per share [EPS], and Unity will flip to positive EPS in early 2023. From an investment standpoint, the move to profitability should lead to continued institutional accumulation, given that some growth funds wait for stocks to post positive earnings growth before building positions. This is evidenced by recent fund flows, with funds holding Unity up more than 50% from Q1 to Q2, and Datadog ownership up sharply as well (997 funds vs. 964 funds). Let's take a closer look at both companies below:

Datadog has multiple products, including Infrastructure Monitoring, App Performance Monitoring, Log Management, User Experience Monitoring, Network Performance, and Security Monitoring. The company is unique in that its observability tools allow IT teams to monitor their infrastructure at any scale, with the data compiled cohesively. The company recently released its Q2 results with another blowout quarter, reporting revenue of $233.6MM, up 67% year/over-year. This was the company's highest growth rate in the past five quarters, with revenue up an impressive ~18% on a sequential basis. Just as impressive, DDOG saw a 58% increase year-over-year in customers with annual recurring revenue above $100,000. Finally, customers using two or more products was up 700 basis points to 75%, with customers using 4+ products nearly doubling to 28%. In total, Datadog now has 16,400 customers with a 130% dollar-based net retention rate and posted free cash flow of $42MM in the quarter.

(Source: YCharts.com, Author's Chart)

These outstanding results have led to an upwards revision in FY2021 and FY2022 annual EPS estimates, with annual EPS expected to grow by more than 33% in FY2021 before accelerating to 46% growth in FY2022 and 51% growth in FY2023. Based on DDOG's compound annual EPS growth rate of ~41% (FY2020 to FY2023), the company is clearly an industry leader and a name worth buying on dips. However, in an exuberant market that's gone 220 trading days without a 5% correction and DDOG trading at nearly 40x sales, it's best to wait for a dip. The ideal buy-point would be a pullback to $118.00 or lower, where the stock would re-test its recent 9-month base breakout and would improve the valuation, leaving DDOG at closer to 34x. So, while I think DDOG is a name worth keeping a close eye on and a clear market leader, I believe the best course of action is waiting for a pullback to add new exposure.

(Source: TC2000.com)

Moving over to Unity, the company had its IPO debut late last year, and its growth thus far has been nothing short of exceptional. In the most recent quarter, U posted revenue of $273.6MM, up 48% year-over-year, and this lapped 42% growth last year, giving the company a 2-year average growth rate of 45%. Notably, this was a more than 11% beat vs. estimates ($243MM), prompting Unity to raise its FY2021 revenue guidance by $45MM. The company noted that the strong results were driven by broad-based strength across all product lines, with its most meaningful growth in Operate and Create. In the Create segment, revenue was up 31% year-over-year to $72MM, while Operate was up 63% year-over-year to $183MM.

(Source: YCharts.com, Author's Chart)

As shown above, Unity continues to see incredible growth on a sequential basis like DDOG, with revenue up more than 16% sequentially in Q2, and revenue on track to grow at a compound annual growth rate of more than 50% vs. Q3 2019 ($130.9MM) based on current estimates. Meanwhile, as the earnings trend below shows, and as alluded to earlier, Unity is expected to flip to positive annual EPS in FY2023, with net losses per share continuing to narrow. As it stands, FY2022 estimates are sitting at a net loss of $0.11 per share, with positive annual EPS of $0.26 in FY2023. On a price-to-earnings basis, Unity appears expensive. However, with a company boasting nearly 50% revenue growth year-over-year, it's actually quite reasonably valued at less than 35x sales, with many high-growth tech companies commanding valuations above 50x sales in their infancy, like Zoom Video (ZM).

(Source: YCharts.com, Author's Chart)

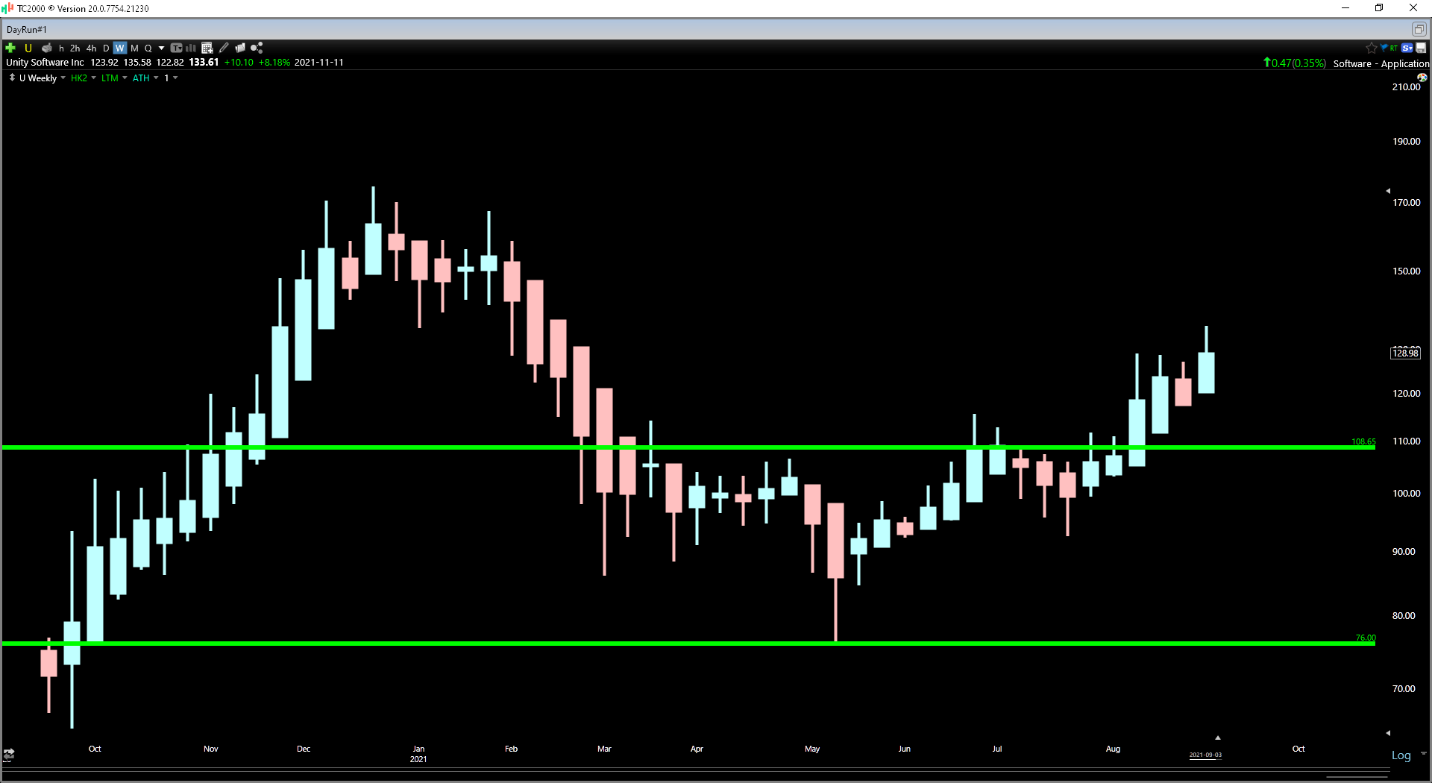

Looking at the technical picture, we can see that U recently broke out of a lower base and has support levels at $108.65 and $76.00. Given that we saw significant buying volume at the recent breakout level and prior resistance levels often become new support levels, I would expect Unity Software to find support if it trades back down to this breakout level. Notably, if we were to see a sharp pullback, this would also significantly improve the valuation, given that U would dip to 25x FY2022 sales estimates of $1.35BB. So, while I have no plans to chase the stock here, I would get very interested in Unity Software if it slides back below the $109.00 level.

(Source: TC2000.com)

In a market where exuberance is the sentiment du jour, it's best not to be greedy, and I believe that some cash preservation is wise. However, if we were to see a sharp pullback later this year in the Nasdaq and S&P-500 (SPY), I believe this would present a decent buying opportunity, as long as a correction can reset sentiment. In summary, while I do not have positions in Unity or Datadog currently, I believe both are very intriguing growth stories worth watching on corrections. The ideal low-risk buy points for starting positions are below $118.00 on DDOG, and below $108.00 on Unity Software.

Disclosure: I have no positions in any stocks mentioned.

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

U shares were trading at $134.91 per share on Tuesday afternoon, up to $1.30 (+0.97%). Year-to-date, U has declined -12.09%, versus a 21.61% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post But the Dip on These Two Tech Stocks With Impressive Growth Rates appeared first on StockNews.com